PROBLEMS SOLVED BY

DUCAT

The Challenge: Locked In bloomberg

Asset managers use Bloomberg EMSX & TSOX for execution,

PORT for portfolio management, and a maze of terminal workflows.

Switching platforms means:

• Retraining staff on new systems

• Rebuilding broker integrations

• Operational disruption & compliance risk

• Enterprise platform costs (Bloomberg, Aladdin, Fidessa pricing)

THE SOLUTION: Augment Bloomberg, Don’t Replace It

DUCAT integrates directly into Bloomberg EMSX and TSOX via FIX protocol and EMSX API.

Your team keeps their terminal, keeps their data, keeps their brokers.

DUCAT adds intelligent execution, portfolio management, and compliance on top.

portfolio Overview holdings

heat MapS

Filter by Asset Class, Compare Holdings & Find Alignment.

- Multi-portfolio, institutional-scale view

- See holdings across all your funds

- Instantly identify over/underweights

- Compare positions and asset class allocations in one place

portfolio Overview

Single Summary heat MapS

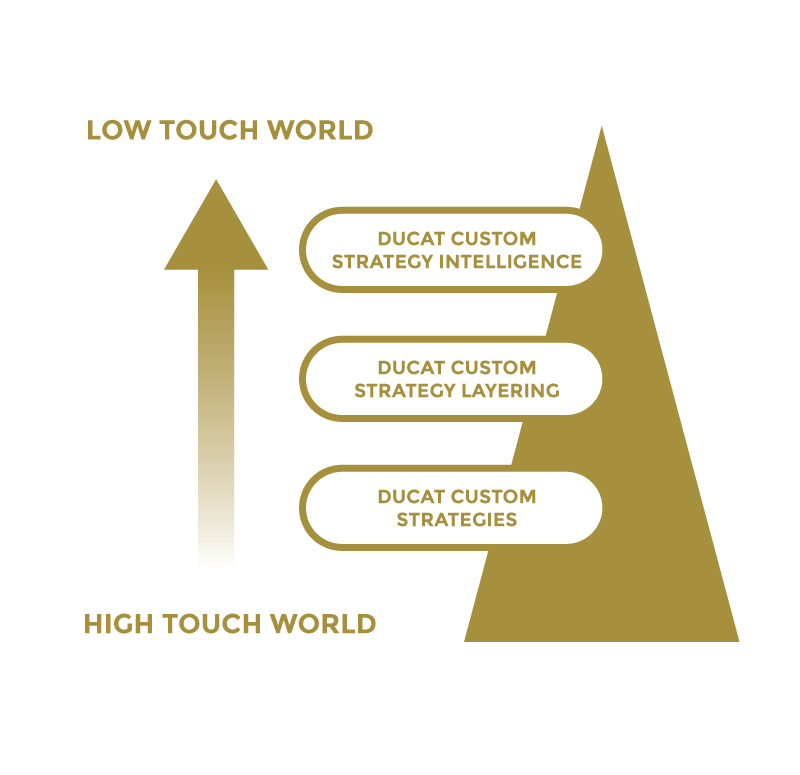

DUCAT custom strategies

Traders now can simply create their own custom, or alternatively use DUCAT preloaded populated strategies, which are specifically mapped to each broker algorithm in their execution management system.

Buy-side traders then are able to place or amend the same instruction across multiple broker algorithms without having to remember or enter each specific broker algorithms input parameters.

The multiple broker algorithm problem faced by buy-side traders

The simple problem hindering extensive use of multiple broker algorithms

It is neither practical nor sustainable for buy-side traders to enter specific algorithm parameters into multiple broker algorithms’ for the bulk of their order book.

What do most buy-side traders need?

Regulatory and client pressure for buy-side traders to lower execution costs and increase best execution transparency through increased use of broker algorithms

To make meaningful shift in bulk of order book from high touch to low touch execution traders need quick and easy 3-steps…

- Select the orders they want traded in broker algorithms

- Select their own custom trading strategy

- Send that instruction to any one of multiple broker algorithms

Why customers choose DUCAT

Solutions to Filter by Asset Class, Compare Holding & Find Alignment.

Enables traders to easily use multiple broker algorithms

Enables traders increased independence to use broker algorithms for more complex trading activities like:

- Managing portfolio in/out flows and re-balances

- Trading underlying securities to linked futures or other index-related linked type trading

- Pairs and hedge fund style strategies

Enables larger proportion of order book traded at lower commission rates

Lowers average execution costs for institutional money managers

Complies to best execution policies as prescribed by MiFID II

DUCAT solves the problem of using multiple broker algorithms

DUCAT custom strategies

Traders now can simply create their own custom, or alternatively use DUCAT preloaded populated strategies, which are specifically mapped to each broker algorithm in their execution management system.

Buy-side traders then are able to place or amend the same instruction across multiple broker algorithms without having to remember or enter each specific broker algorithms input parameters.

DUCAT multiple custom strategy layering

Using DUCAT Algorithm Manager, traders are able to place MULTIPLE broker algorithm orders, which are defined in a SINGLE custom input template

Simple examples include placing 3 simultaneous broker algorithm orders, one which trades targeting VWAP, a second which participates when last price is for example better than 20bps from interim VWAP, and a third order which participates when last price is for example 40bps better than interim VWAP

DUCAT custom strategy intelligence

Using DUCAT Algorithm Manager, traders are able to create execution strategies which AMEND broker algorithm input parameters automatically according to predefined market or order events

Examples include custom DUCAT market volume participation strategies which amend broker algorithm price limit parameters according to interim order VWAP or market VWAP metrics